Does the resurgence of worth shares over development shares imply the bull market’s days are numbered?

I’m referring to the epic battle between two main inventory market types: development shares (these of corporations which are rising the quickest and are buying and selling for greater valuations) and worth shares (out of favor corporations which are buying and selling for decrease valuations).

Whereas worth shares on common over the previous century have considerably overwhelmed development, they’ve suffered important durations throughout which development has come out on high. The previous decade has been one such interval.

The tide started to show within the fall of 2020 in favor of worth, inflicting widespread celebration amongst worth managers that perhaps — simply perhaps — their lengthy interval of struggling was ending. Most different managers regarded on with bemused attachment, contemplating the growth-versus-value debate to be little greater than an intramural rivalry.

Some observers suppose that angle is shortsighted. They consider that development shares’ fortunes relative to worth shares could inform us whether or not or not we’re in a wholesome bull market.

On the floor their argument is smart. Development shares presumably can be rising the quickest when the economic system is firing on all cylinders. And financial development is definitely conducive to a bull market on Wall Avenue. So it stands to motive {that a} shift in management to worth from development would possibly signify an imminent market downturn.

This theoretical argument accords with the inventory market’s expertise main as much as, and following, the bursting of the web bubble in 2000. The bull market years of the Nineties had been one of many longest durations over the previous century through which development shares beat worth. After that bubble burst, worth shares started one of many longest durations over the previous century through which they beat development.

There are exceptions within the historic report. Through the Nice Monetary Disaster, for instance, development shares on stability outperformed worth. But the economic system shrunk considerably and the inventory market plummeted.

What the info inform us

To get a greater deal with on this complicated relationship between the market’s well being and growth- and worth shares’ relative returns, I analyzed the inventory market’s tendencies again to mid-1926, courtesy of information from Dartmouth professor Ken French and Yale University professor Robert Shiller. For every month I obtained knowledge on worth’s efficiency relative to development, in addition to the S&P 500’s

SPX,

inflation- and dividend-adjusted efficiency.

I looked for correlations between the 2 and got here up empty. There have been some durations through which worth’s relative energy was related to decrease inventory market returns, and others through which it was correlated with greater returns. There was no constant sample.

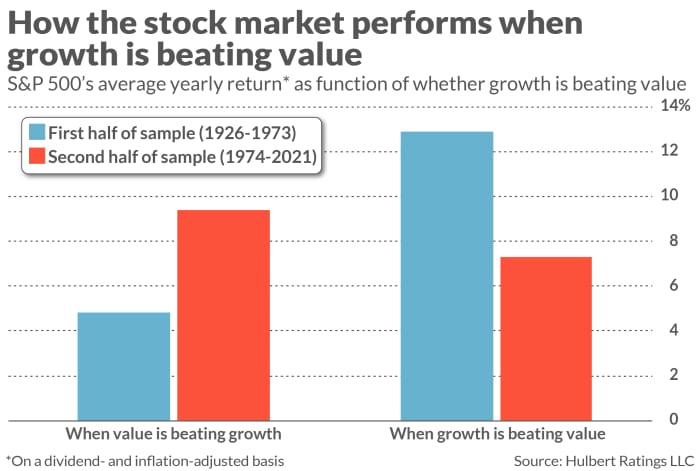

That is illustrated within the chart above. It breaks the info into two equal-sized teams — the primary encompassing the 1926-1973 interval, and the second the interval from 1974 till now. Within the first half of the pattern the inventory market did higher when development was beating worth. It was simply the reverse within the second half of the pattern.

My hunch as to why there may be an inconsistent correlation between the market and worth’s relative energy in opposition to development: There’s a couple of motive why development can slip behind worth. The energy of the economic system is however one motive. One other, which has turn out to be significantly related in current many years, is a bubble in growth-stock valuations. If such a bubble deflates, development shares can critically lag worth shares even whereas the general economic system continues to develop.

We noticed a few of this in the course of the deflation of the web bubble between March 2000 and October 2002. Although that bear market lasted two-and-a-half years, the related recession lasted simply eight months (from March to November 2001, according to the National Bureau of Economic Research, the semi-official arbiter of when recessions begin and end). On the finish of that bear market, U.S. gross home product (GDP) was 10% greater than the place it stood initially. But the S&P 500 was 49.1% lower. A lot of that distinction might be chalked as much as development inventory valuations coming again to earth.

Worth shares carried out fairly effectively throughout that bear market, in relative phrases. Moreover, in accordance with French’s knowledge, the common small-cap worth inventory truly made cash throughout that bear market.

The underside line? Loosen up. Whereas a lot is driving on whether or not the worth model has launched into a several-year interval of outperforming development, the destiny of the bull market is just not one in every of them.

Mark Hulbert is an everyday contributor to MarketWatch. His Hulbert Scores tracks funding newsletters that pay a flat payment to be audited. He might be reached at mark@hulbertratings.com

Extra: Why stock market bulls may be right to push valuations so high

Plus: Not every stock is in a bubble. Here’s how to find today’s bargains and tomorrow’s winners

{kind=link}